Related Articles

3 things to stop doing today to get the job of your dreams

The Recruiter's Perspective: how to answer...

Group Work & Team Presentations (Video)

Reading & Research (Video)

How to answer "What was your greatest disappointment?"

Profitability Framework

Commercial Awareness (Video)

See More...

11 February 2016 |

Profitability Framework

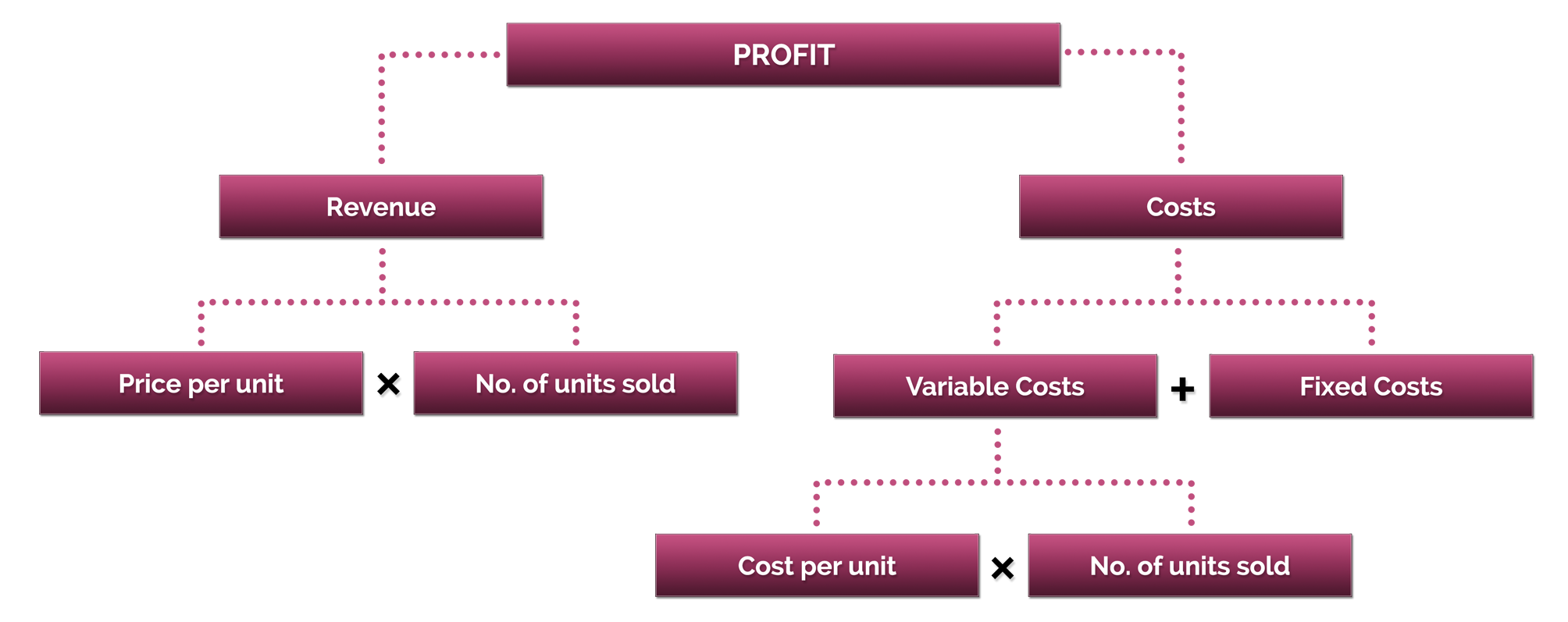

The Profitability Framework is probably the most frequently used quantitative framework in case interviews so familiarise yourself with its component parts. It can be applied to any case that relates to changes in either revenues generated or costs incurred by a business. Consultants are frequently engaged to help clients tackle issues relating to profitability. For instance, clients may have experienced a drop in sales or may be struggling to control their costs. A consultant would need to identify the exact source of the problem(s) and subsequently deliver proposed solutions.

The Framework

Questions You May Be Asked

1. Company ABC has been facing a decline in its sales figures over the past 3 years. What can they do in order to reverse the trend and get back on the right growth path?

2. Your client is a candy manufacturing company that has been facing falling profit margins. The CEO has reached out to us to figure out why and what they should do about it.

Analysis

It is important to walk your interviewer through each step you take when applying the Profitability Framework to a case study. Explain which ‘branches’ of the framework you are considering (e.g. the ‘Costs’ or ‘Revenues’ branches). If you decide to switch branches, explain why you have decided to do so. Start by stating that the two main components of profitability are revenue and costs and that the difference between these two metrics gives you the profit figure. If your interviewer has not specified whether the company has a revenue or costs problem, you should ask him or her whether either (or both) of these two metrics have changed.

Revenue

- If revenues have decreased and costs have not changed, this suggests that the issue relates to revenues. Your next step should therefore be to assess the branches underneath ‘Revenues’ in order to determine whether that change is the result of a fall in the price per unit or a fall in the number of units sold.

- If however revenues have remained stable but costs have increased, you should ‘drill down’ the ‘Costs’ branch instead (i.e. assess the sub-branches linked to the ‘Costs’ branch).

- The total cost figure depends on both variable and fixed costs, so you need to determine which of the two types of costs has increased.

- If variable costs have increased, then drill down further to determine if the change relates to the cost per unit or the number of units sold.

- If fixed costs have increased, you may have to segment the fixed costs to see whether a certain type of fixed cost has increased to an unsatisfactory extent.

- Remember that an increase in fixed costs may indicate investment has taken place (e.g. investment in new plant & machinery), which in the long-term could increase revenue and improve profitability (even if profitability has been negatively impacted in the short-term).

Costs

A drop in profitability may sometimes be driven by a combination of changes on both the revenues and costs sides. If this is the case, you should drill down both branches (separately) until you find the source(s) of the problem. If the interviewer specifies that the case study strictly relates to one branch in particular, you can focus on that specific branch. Depending on the company’s objective in a particular case study and the style of interview, you may next be expected to move onto the Business Situation Framework. This can help you to structure your analysis of important qualitative factors that may have had some influence over the issue(s) the company is facing (e.g. whether the issues are industry-wide or company-specific). There are various strategies that businesses can employ to minimise or stabilise costs. For instance: maximising economies of scale; integrating into the supply chain; outsourcing; offshoring; entering long-term contracts; using Just-In-Time Production strategies and utilising derivatives.